Imagine a Tuesday morning at a fish farm along the coasts of Norway or southern Chile. The coffee is hot, but the screens display a cold reality: the spot price of salmon in the physical market has just plummeted. For a producer, this scenario is a recurring nightmare. You have spent months feeding your fish, investing in oxygenation, and navigating biomass regulations—only for the market to swing unpredictably just as they are ready for harvest.

For nearly two decades, financial instruments known as futures contracts—initially traded on the Fish Pool exchange and recently transitioned to Euronext Paris—have promised to be the ultimate shield against these pricing storms. Yet, many producers and technicians view these markets with skepticism, mistaking them for a speculative casino or, worse, relying on theoretical analyses that fail to reflect the day-to-day realities on the water.

This is precisely where economic science comes to our rescue. A groundbreaking recent study by researcher Daumantas Bloznelis from the Norwegian University of Life Sciences, published in the scientific journal Aquaculture Economics & Management, dismantles several deeply rooted myths about how salmon finance actually behaves. The result is an invaluable guide for entrepreneurs, risk managers, and operators to understand exactly when and how to lock in prices to safeguard their profits.

- 1 Why Desk Math Failed on the Water

- 2 Research Is a Human Process (Flaws and All)

- 3 The Two Great Revelations That Will Transform Your Commercial Strategy

- 4 The Market Anatomy: Seasonality is the Key

- 5 From Theory to Practice: A Trading Strategy

- 6 Conclusion: Returning to the Farm with Secured Profits

- 7 Entradas relacionadas:

Why Desk Math Failed on the Water

For years, traditional financial analysts have relied on standard mathematical models, such as the Capital Asset Pricing Model (CAPM), to assess salmon risk. The problem is that these models were originally designed for Wall Street—tailored for stocks like Apple or Coca-Cola, not for living organisms growing in marine cages and subjected to seasonal cycles.

A previous study (Ewald et al. 2022) asserted that salmon futures behaved predictably and offered no abnormal returns. However, the operational reality of aquaculture farms contradicts these academic theories. Bloznelis discovered that prior analyses suffered from two major flaws: they calculated risks on a week-by-week basis—which is ineffective in a market where days can pass without a single contract being traded—and they erroneously assumed that price variations remained constant whether a kilo of salmon cost 4 or 10 euros.

Consequently, Bloznelis redesigned the equations. Instead of looking at raw monetary gains week over week, he shifted his economic lens to analyze monthly relative returns. By adjusting the model to reflect the actual low liquidity of the market—meaning the speed and ease with which contracts can be traded without driving down prices—the data revealed something remarkable: the salmon market hides repetitive, predictable patterns that a shrewd producer can exploit to either generate profit or hedge their investment with surgical precision.

Research Is a Human Process (Flaws and All)

Economic science is not perfect, and Bloznelis demonstrates this with complete transparency in his paper. Gathering 18 years of historical data from Fish Pool—spanning from 2006 to 2024—was a Herculean task, as the researcher confronted a market he characterizes as “chronically illiquid.”

“On a traditional stock exchange, thousands of transactions occur every second. In the salmon futures market, during its first nine years, a contract for a specific date was traded, at best, twice a month; and volumes did not change significantly until 2024.”

This lack of continuous trading creates a technical hurdle that economists dread: the data becomes “noisy” and heteroscedastic (a sophisticated term meaning that volatility changes size unpredictably). Traditional statistical methods yielded biased results. To overcome this roadblock, the researcher had to design custom statistical tools—dubbed HACseas and HCseas—and apply computational simulations called bootstrapping to ensure the findings were as robust as the netting of an offshore sea cage. Thanks to this rigorous effort to correct the flaws of older models, we now possess a clear pricing roadmap.

The Two Great Revelations That Will Transform Your Commercial Strategy

Bloznelis’s analysis, which integrated both the CAPM and the robust Fama-French three-factor model, yielded two primary conclusions that every technician and producer must memorize:

Stay Always Informed

Join our communities to instantly receive the most important news, reports, and analysis from the aquaculture industry.

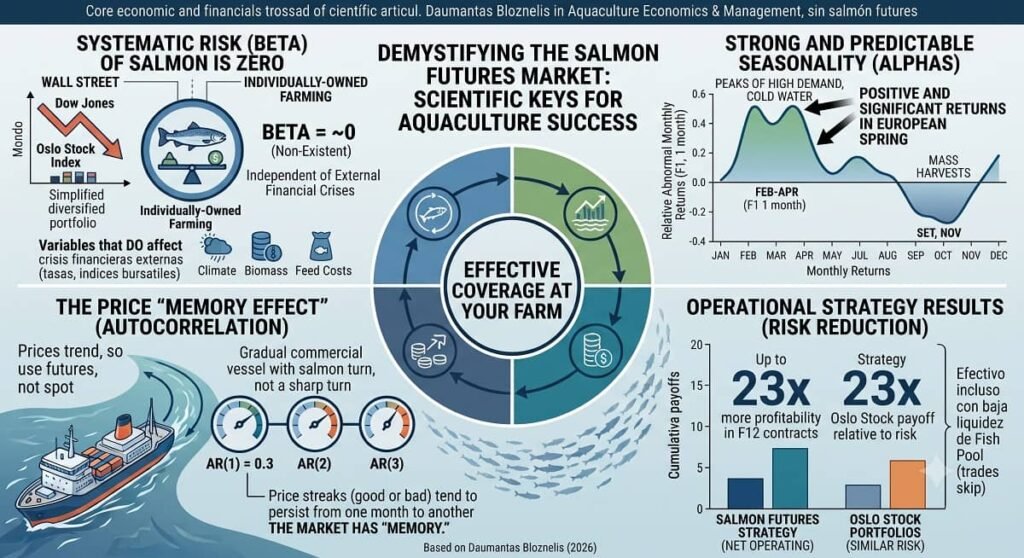

Salmon Swims to Its Own Rhythm (Near-Zero Systematic Risk)

In finance, “systematic” risk, or beta, measures how exposed a business is to the fluctuations of the global economy or the stock market. If Wall Street crashes, most stocks go down with it. However, the study demonstrated that the beta of salmon futures is practically zero. In practice, this means the price of your fish does not depend on whether tech stocks rise or fall, nor on central bank interest rates. Salmon is driven by its own unique variables: weather conditions, smoltification success, algal blooms, government biomass quotas, and feeding cycles. For an entrepreneur, this is a distinct advantage: it means investing in salmon is an excellent diversification strategy, acting as a shield that remains immune to traditional financial crises.

The “Memory Effect” (Positive Autocorrelation)

This is the study’s most disruptive finding. Bloznelis discovered a strong first-order autocorrelation of approximately 0.3 across all futures contracts (from month 1 to month 12). To put it simply: salmon prices possess a “short-term memory.” If a futures contract’s return was positive last month, there is a very high statistical probability that it will remain positive this month. This challenges the “efficient market hypothesis,” which argues that tomorrow’s prices are completely unpredictable. In the salmon sector, trends do not reverse overnight; they move like a massive cargo ship that takes time to slow down and turn around.

The Market Anatomy: Seasonality is the Key

To visualize how these forces interact, let us analyze the structure of the extended model proposed by the study. You do not need to be a mathematician to understand how your pricing security operates:

| Analyzed Factor | Actual Market Behavior | Impact on Your Aquaculture Farm |

| Market Risk (Beta) | Near-zero (Nonexistent) | Your contracts remain immune to external financial crises. |

| Memory Effect () | Strong and positive (~0.3) | Pricing streaks (whether favorable or adverse) tend to persist month over month. |

| Seasonality (Alphas) | High returns in February–April; declines at year-end | The biological cycle defines optimal time windows to sell futures. |

To understand “seasonal Alphas”—those abnormal returns detected in the study—let us use a biological analogy. Imagine your company’s commercialization strategy functions like the farm’s security team: if you know that thieves are more active during the winter, you reinforce your lighting during that specific season.

In the salmon market, the study rigorously demonstrated that February, March, and April register abnormally positive returns on short-term contracts (). This occurs because it coincides with the end of the European winter, when colder waters slow fish growth, the supply of fresh salmon drops, and demand drives prices upward. Conversely, September and November tend to yield negative returns due to the surge of massive late-summer harvests.

From Theory to Practice: A Trading Strategy

Does all of this have a real impact on profitability, or is it just theory to be archived? To prove it, Bloznelis conducted a bold experiment: he designed a real-time trading simulation strategy based on his 10-year rolling-window findings. The rule was simple: if the model predicted a positive abnormal return for the next month due to the memory effect and seasonality, a contract was purchased (long position); if it predicted a decline, it was sold (short position). To maintain strict risk control, profits were never reinvested, and only one contract was traded at a time.

The net results—after deducting all transaction costs and operational fees—were astonishing. The strategy applied to salmon futures generated average monthly returns that overwhelmingly outperformed stock portfolios of similar risk on the Oslo Stock Exchange. For certain long-term contracts ($F_{12}$), salmon profits were up to 23 times higher than those of the conventional stock market. The author prudently warns that, due to the low liquidity of the salmon exchange, some trades could not have been executed on time in real life; however, even if an aquaculture producer had been forced to discard half of the transactions due to a lack of buyers or sellers, the final profitability would still have remained considerably higher than any traditional financial investment.

Conclusion: Returning to the Farm with Secured Profits

Let us return to the Tuesday morning that opened this article. The screens still show that the physical (spot) salmon price is plummeting, but this time, the atmosphere in the farming facility’s office is completely different. Because the management and technical teams now understand the science behind futures, the company is not left unprotected. Three months ago, in the dead of winter—leveraging the knowledge of positive seasonal Alphas and the memory effect described by Bloznelis—the commercial manager signed futures contracts to lock in the price of today’s harvest. While traditional producers suffer losses trying to sell their fish in a rush on the physical market, your farm executes its pre-established financial contracts, keeping profit margins intact.

Scientific research demonstrates that the salmon futures market is neither hostile territory nor an indecipherable mystery; it is a tool governed by clear biological and financial rules. Understanding that stock market risk does not affect your fish and learning to read monthly trends will give you absolute control over the economic future of your biomass. The next time the spot price drops, make sure your only worry is the water temperature.

Contact

Daumantas Bloznelis

School of Economics and Business, Norwegian University of Life Sciences

Ås, Norway

Department of Business Administration, Inland School of Business and Social Sciences, University of Inland Norway

Rena, Norway

Email: daumantas.bloznelis@nmbu.no

Reference (open access)

Bloznelis, D. (2026). Explaining salmon futures returns with factor models. Aquaculture Economics & Management, 1–35. https://doi.org/10.1080/13657305.2026.2690911

Editor at the digital magazine AquaHoy. He holds a degree in Aquaculture Biology from the National University of Santa (UNS) and a Master’s degree in Science and Innovation Management from the Polytechnic University of Valencia, with postgraduate diplomas in Business Innovation and Innovation Management. He possesses extensive experience in the aquaculture and fisheries sector, having led the Fisheries Innovation Unit of the National Program for Innovation in Fisheries and Aquaculture (PNIPA). He has served as a senior consultant in technology watch, an innovation project formulator and advisor, and a lecturer at UNS. He is a member of the Peruvian College of Biologists and was recognized by the World Aquaculture Society (WAS) in 2016 for his contribution to aquaculture.

: Complete care guide for aquarium, eeding, breeding, and common illnesses")